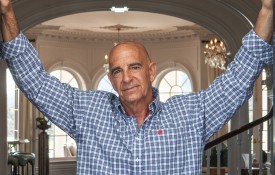

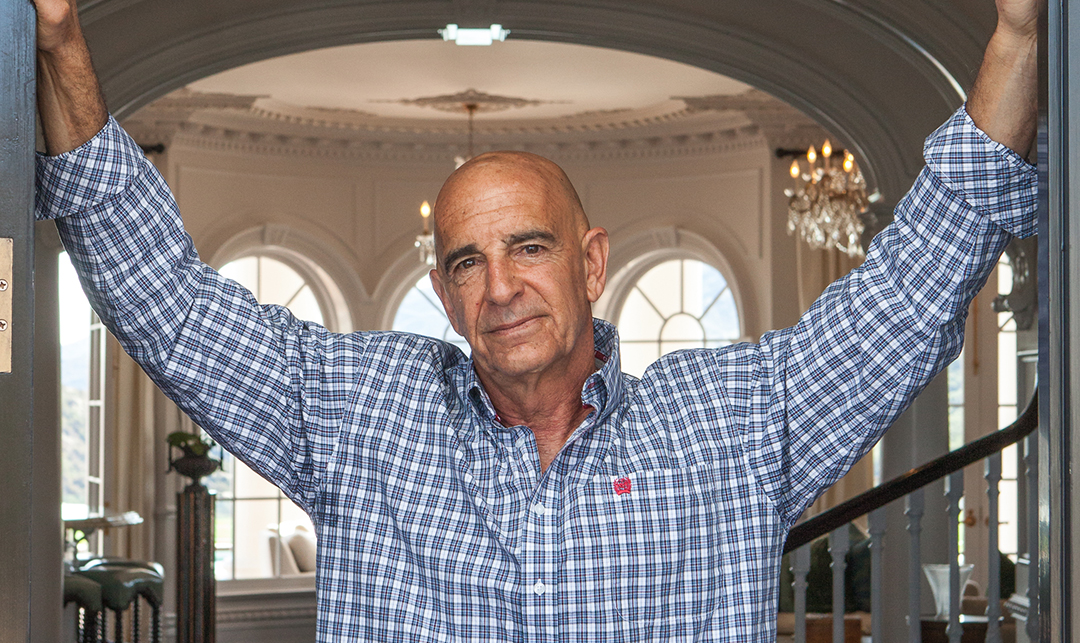

Howard Marks has said on multiple occasions that his financial philosophy is rooted in controlling risk. So it’s ironic that his company, Oaktree Capital Management, is the world’s largest investor in distressed debt. He is quick to point out that this represents only a portion of the company’s dealings, but given Oaktree’s track record of lucrative success in returning struggling companies to financial viability through restructuring, it’s no surprise that Marks himself has come to be known as somewhat of an investment guru.

This reputation is fortified by his advocacy of second-level thinking: the idea that taking the opposite action of popular public opinion may be the most prudent and intuitive approach to investing. In his book, The Most Important Thing: Uncommon Sense for the Thoughtful Investor (2011, Columbia University Press), Marks explains:

First-level thinking says, ‘It’s a good company, let’s buy the stock.’ Second-level thinking says, ‘It’s a good company, but everyone thinks it’s a great company, and it’s not. So the stock’s overrated and overpriced; let’s sell’ [or] First-level thinking says, ‘The outlook calls for low growth and rising inflation. Let’s dump our stocks.’ Second-level thinking says, ‘The outlook stinks, but everyone else is selling in panic. Buy!’ (p. 3)

Another simple pearl of financial wisdom Marks has dispensed declares, “If we avoid the losers the winners take care of themselves.” In essence, that means clients don’t mind if his company does slightly less than the average in bullish times (because they’ll still be making money), as long as they can rest assured of doing much better than average during bear times.

“Make sure you have good reasons for [going public] so that you can explain to your constituencies, because it may cause them to have fears that you’ll be more focused on satisfying Wall Street than on what’s in your clients’ best interest.”

Formed in 1995 by a group of individuals who had been investing together in high-yield bonds, convertible securities, distressed debt, real estate, and control investments since the mid-1980s, Oaktree Capital has enjoyed a nearly continuous run of success. The company went public in 2012 and has a market cap of $8B as of March 2015.

We asked him for an insider’s perspective of the process, including lessons learned from an IPO offering. “On the positive side, many companies will go public if they need capital to expand,” he points out. “In our case, it gave us the ability to sell some of the stock to the public at a fair market price, and that facilitated a generational transition of ownership from us to the next generation of Oaktree leaders.” Regarding the negative side of going public he advised, “Make sure you have good reasons for doing it so that you can explain to your constituencies, because it may cause them to have fears that you’ll be more focused on satisfying Wall Street than on what’s in your clients’ best interest. You can deal with that by having a deeply trusting relationship with your clients, which is something you should have been building all along.”